Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

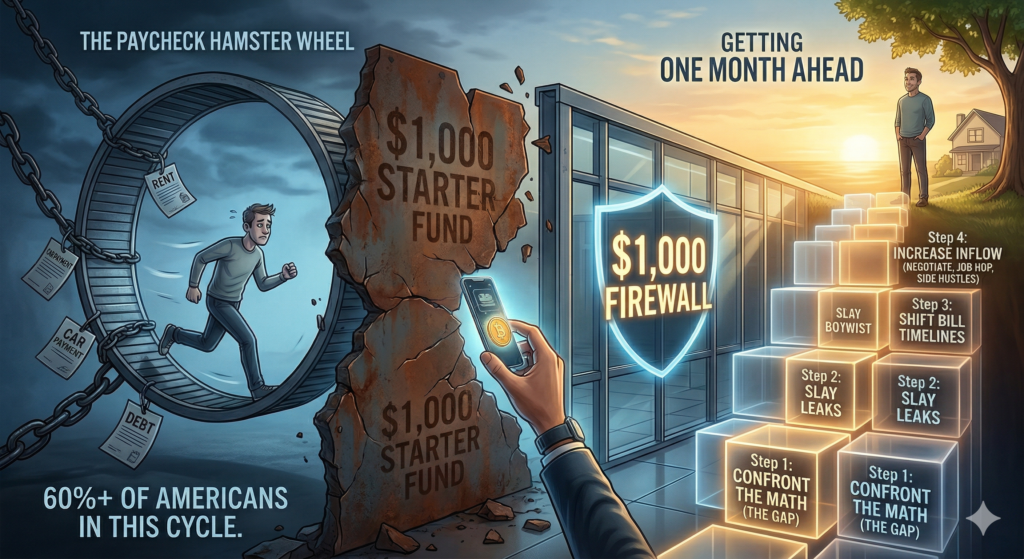

Let’s start with a validating reality check: If you are living paycheck to paycheck right now, you are in the majority. Financial surveys consistently show that upwards of 60% of Americans are caught in this exhausting cycle—and it includes a surprising number of six-figure earners.

The standard advice to “just stop buying coffee” feels tone-deaf when grocery and housing costs are skyrocketing. Breaking this cycle isn’t about guilt; it’s about building a bulletproof money game plan. Here is a realistic, step-by-step guide to finally getting off the financial hamster wheel.

You cannot fix what you refuse to measure. The cycle exists for one simple reason: there is no gap between what flows into your bank account and what flows out.

Block out 20 minutes for a “Bleed Audit.” Look at your actual take-home pay, then categorize your expenses into Fixed Survival Costs (rent, basic groceries, minimum debt payments) and Variable Lifestyle Costs (takeout, subscriptions, hobbies). If your fixed costs are reasonable but your variable costs eat the rest, you have a behavioral spending problem. Knowing your baseline is step one.

Forget saving six months of living expenses right out of the gate. When you have $14 left three days before payday, that goal is entirely demoralizing.

Your only mission right now is a $1,000 starter emergency fund. This covers minor everyday catastrophes—a blown car alternator or an urgent care visit—that usually force you to reach for a credit card. Keep this firewall in a separate, high-yield savings account to protect you from high-interest debt traps.

Wealth doesn’t usually vanish in grand purchases; it bleeds out in $15 increments. Today, convenience is the ultimate tax on our wealth.

Do a subscription purge today: cancel every streaming service or app you haven’t used in the last two weeks. Next, tackle meal planning. We usually spend money on takeout because we are tired at 6:00 PM and have no plan. Spending just 20 minutes mapping out your meals can realistically save you hundreds a month.

Sometimes the issue isn’t a strict lack of money, but a lack of cash flow management. If all your major bills hit on the 1st of the month, your first paycheck is wiped out immediately, leaving you broke for two weeks.

Call your utility companies and lenders to change your billing dates so your expenses are evenly distributed across your pay periods. This prevents those artificial periods of poverty right before your next check.

There is a mathematical limit to how much you can cut; you simply cannot out-budget a fundamentally low salary. Once you’ve slashed expenses, focus on the income side of the equation.

Negotiate a raise, look for a higher-paying role, or start a strategic side hustle. Don’t just burn yourself out driving rideshare all weekend unless it’s a temporary sprint to fund your $1,000 firewall. Look for scalable opportunities—like launching an e-commerce storefront for niche physical products, or freelance consulting—where your specialized skills command a much higher return on your time.

Breaking the paycheck-to-paycheck cycle is about making small, consistent decisions over several months. It requires the discipline to audit your spending, build a cash buffer, and aggressively grow your income. It isn’t easy, but the peace of mind that comes from knowing exactly how you will pay for next month is worth every single ounce of effort.